August 29, 2023

Jacob Celermajer, Portfolio Manager

Key takeaways:

• Sub-sectors of the medtech industry tend to form into natural oligopolies due to deep and wide economic moats.

• Medtech companies typically have strong pricing power due to this competitive dynamic.

• This oligopolistic industry structure has driven a period of strong risk-adjusted returns that we believe is likely to continue over the long-term.

In the Cordis Global Medical Technology Fund, we have built out an investment opportunity in which we believe the deck is already stacked in our client’s favour. We have previously discussed the insatiable demand for medtech that is driving top-line revenue, and in this article we outline the medtech industry’s natural tendency towards oligopolies, which drives earnings and ultimately share prices.

While each sub-sector within medtech has its own competitive dynamics and structural nuances, there has always been a trend for early players to corner the market. This is in the most part due to extremely high barriers to entry – also known as economics moats – that protect the early-to-market device developers. This first mover advantage often renders the time, effort and up-front cash required for sub-scale players too onerous. And unlike in the pharmaceuticals industry, there is no market for generic low-cost alternatives in the world of high consequence medical devices. The key barriers/moats that protect medtech incumbents include:

- Development & regulatory; medical device development requires costly up-front investments in research, development and clinical trials

- Brand reputation; a critical factor in an industry literally dealing in life and death

- Intellectual property protection; patent holders are granted a temporary monopoly when coverage is broad enough

- Distribution networks; the ability to get devices into the hands of physicians and operators

- Economies of scale; manufacturing cost advantage makes it difficult for smaller companies to compete

The natural oligopolistic structure is then further perpetuated by the industry standard practice of tuck-in M&A. Typically, large established medtech conglomerates will seed fund early-stage medtech ventures to guarantee first right-of-refusal to buy and own intellectual property should the technology develop into a winner. This plays out in fewer bigger competitors dominating the market.

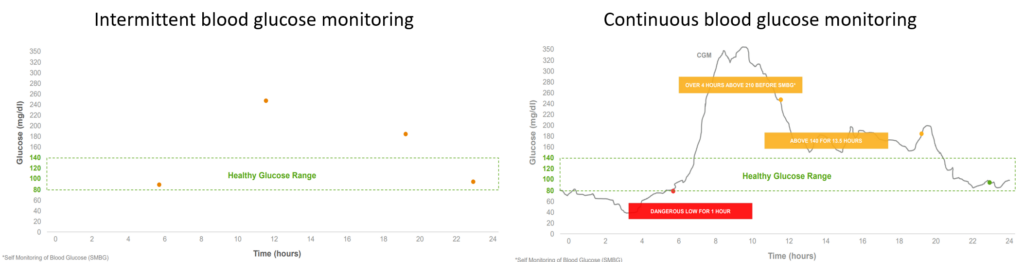

A pertinent example of a medtech oligopoly is the market for blood glucose monitoring technology, a space in which the Cordis Global Medical Technology Fund has significant positions. CGMs (continuous glucose monitors) have been one of the most important steps forward in the treatment of diabetes in the past 20 years. The ability to track glucose continuously, rather than intermittently, has allowed patients with diabetes to better pre-empt and therefore treat their condition, all without the requirement for painful and socially burdensome finger-sticking to obtain a blood sample.

The first continuous glucose monitor was approved all the way back in 1999, and despite almost 25 years of progress, the market remains a three-way oligopoly today where the leading players hold >95% of global market share. These three key players – DexCom (DXCM:NASDAQ), Abbott (ABT:NYSE) and Medtronic (MDT:NYSE) – have used this 25-year head start to build deep customer relationships, expansive distribution networks, efficient manufacturing scale and comprehensive clinical data that will protect them against new competition for many years to come.

An even more profound example is in the surgical robotic space, where Intuitive Surgical (ISRG:NASDAQ) – the global leader in surgical robotic systems – maintained a natural (non-regulated) monopoly for over 15 years. Its first generation da Vinci system was approved for general surgery by the U.S. FDA (Food and Drug Administration) in 2000 and remained the only approved device until 2017, as other players struggled to overcome the R&D hurdles that Intuitive overcame in the early 2000s. In the 17 years of monopoly operation, Intuitive’s stock returned over 5,800%, or greater than 25% per annum. In the period of duopoly operation since, Intuitive has continued to return in excess of 15% annually for shareholders1. As more competition comes to market, new players with little track record will find it very tough to compete with Intuitive’s body of clinical evidence, which includes a global network of 8,000 da Vinci systems that have performed 13 million procedures and over 34,000 peer reviewed published articles2. Intuitive’s trusted brand reputation is likely to remain a key competitive advantage against new upstart competitors long into the future.

This favourable competitive landscape affords medtech companies the ability to be price makers, rather than price takers. Gross margin is our favoured indicator of pricing power, as it evidences a company’s ability to set the price level, based around competitive market forces and the need or desirability of a given product. Medtech’s customers – which are typically governments or private insurers – willingness to pay these higher prices is the first layer of defence when building up a firm’s profitability. This ability to pass on price is also an important characteristic in protecting earnings during inflationary periods and supported the medtech industry through the recent period of high inflation. These characteristics have manifested themselves in the Cordis Global Medical Technology Fund, which has a weighted average gross margin of 64%, well above that of the S&P Global 1200 Healthcare, S&P Global 1200 and S&P ASX200, with marks of 58%, 51% and 46% respectively1.

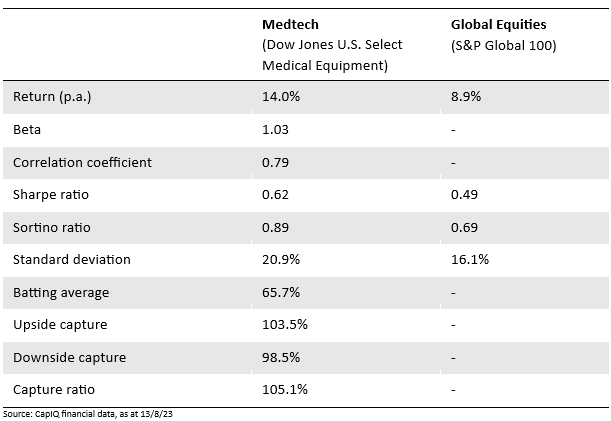

The nature of this industry structure has led the medtech sector to a period of significant outperformance, as illustrated by using the Dow Jones U.S. Select Medical Equipment Index as a sector proxy. Since its inception in 2006, the index has outperformed the global equities market, as represented by the S&P Global 100.

During this history of long-term outperformance, the medtech sector has also delivered on a risk-adjusted basis. Although absolute volatility – as measured by the standard deviation – is higher, the excess returns translate into significantly higher Sharpe and Sortino ratios.

The returns generated by medtech have also been consistent rather than unpredictable and lumpy. The batting average suggests that medtech outperforms the market approximately two thirds of the time, while the capture ratios indicate that medtech typically rises by more and falls by less than the broader share market.

With little to suggest the growth momentum evident today in medtech will be derailed, exposure to medtech remains one of the few avenues for investors to capture resilient growth that is largely independent of economic cycles, to deliver very attractive risk-adjusted returns.

1. CapIQ financial data, as at 23/8/23

2. Intuitive Surgical Q2 2023 Investor Presentation, 20/7/2023

Disclaimer

This report was prepared by Cordis Asset Management Pty Ltd ABN 68 637 078 490 a corporate authorised representative (No. 1282680) of Avenir Capital Pty Ltd ACN 150 790 355, AFSL 405469 (“Cordis”)”, the investment manager for the Cordis Medical Technology Fund (“Fund”). Equity Trustees Limited (“Equity Trustees”) ABN 46 004 031 298 AFSL No. 240975, is a subsidiary of EQT Holdings Limited ABN 22 607 797 615, a publicly listed company on the Australian Securities Exchange (ASX:EQT), and is the Responsible Entity of the Fund. This document has been prepared for the purpose of providing general information only, without taking account of any individual person’s investment objectives, financial circumstances or needs. Whilst every care has been taken in the production of this document, no warranty is given as to its accuracy and persons relying on this information do so at their own risk. The information contained in this document is not intended to be relied upon as a forecast and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy, nor is it investment advice. Any forwarding-looking statements or forecasts are based on reasonable assumptions, but cannot be relied upon as guarantees or representation as to what future performance will actually occur. Unless otherwise specified, the information contained in this document is current as at the date of issue and all amounts are in Australian Dollars (AUD). You should consider the Product Disclosure Statement (“PDS”) in deciding whether to acquire, or continue to hold, the product. A PDS and application form is available at www.cordisam.com. Cordis and Equity Trustees do not guarantee the performance of the Fund or the repayment of the investor’s capital. To the extent permitted by law, neither Equity Trustees, Cordis, nor any of their related parties including its employees, directors, consultants, advisers, officers or authorised representatives, are liable for any loss or damage (including consequential loss or damage) arising directly or indirectly as a result of reliance placed on the contents of this report. Past performance is not indicative of future performance. The unit price performance calculation methodology follows the FSC Standard No.6: Investment Option Performance – Calculation of Returns (July 2018). Total returns are calculated based on changes in net asset values, at the exit price after the deduction of fees and expenses. Due to individual circumstances, your net returns may differ from the net returns quoted above.