September 1, 2023

Michael Cartmill, Co-Founder and Medical Device Analyst

Key takeaways:

• GLP-1s are gaining more investor focus, but these drugs have been around medical and scientific circles for over 5-years.

• Evidence for GLP-1s is strong, but there are some concerns in the near-term limiting wide-spread population use.

• Even with the success of GLP-1s, there remains one risk factor that medical science is still searching for solutions to – ageing.

Perhaps not since statins, the cholesterol lowering drugs introduced in the 1980s, showed their efficacy at reducing the risk of heart attack, has there been more excitement about a class of drugs as there is currently for GLP-1s (Glucagon-Like Peptide-1). That hype for statins was justified; global sales are now reported to be near US$20 billion annually1.

GLP-1s are a class of drug developed to manage blood sugar levels in type 2 Diabetics. These drugs are designed to have the same effect as a naturally occurring hormone that is released into the bloodstream in response to eating. Their main mechanism is to signal to the pancreas to release more insulin, allowing the body to utilise its sugar as a source of energy. High blood sugar is particularly harmful, leading to chronic diseases such as obesity, heart attacks and strokes.

A simplistic explanation is that GLP-1s ‘trick’ the body into believing that it has just ingested a large, calorie-rich meal, reducing the urge to eat more or to draw on energy reserves.

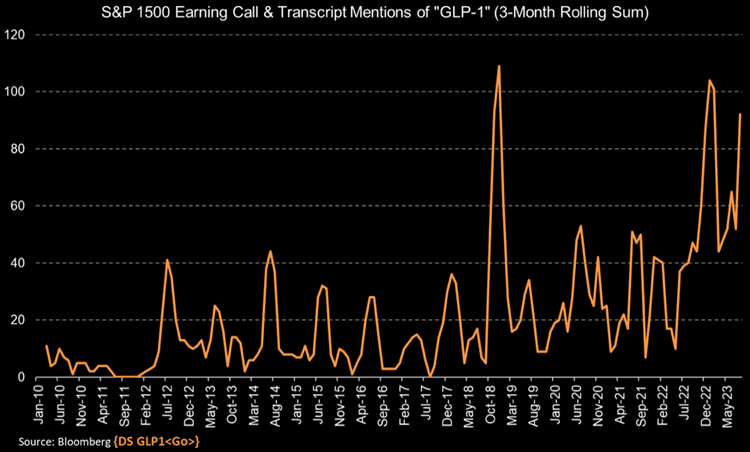

While these drugs have been around for some time, it is only now that excitement is spreading beyond the fields of science and medicine and into the financial markets. According to Bloomberg data, the number of mentions of “GLP-1” in earnings-call transcripts has more than doubled compared to the same period last year2.

GLP-1s, more commonly referred to by their brand names – Wegovy, Ozempic, Mounjaro and others – likely have come into investor focus due to the drip feed of clinical data reaching a tipping point with a few recent positive read-outs.

In late May, Pfizer announced strong weight loss data from a trial of their danuglipron drug, an oral GLP-1 (as opposed to injections like Ozempic and Wegovy). Then, in early August, Novo Nordisk announced 5-year data from their SELECT trial of Semaglutide, showing that Wegovy caused a 20% reduction in major adverse cardiovascular events. Finally, in late August, a University of California, Irvine study on Wegovy presented data suggesting that up to 43 million fewer Americans would present with obesity over the next decade. (Although, it must be said that the UC Irvine study is simply a recalculation of the predicted number major cardiac events assuming the risk reduction from patients being less obese.)

While the evidence for GLP-1s is strong, there are some concerns in the near-term limiting wide-spread population use:

- The drugs are still new and relatively early in their lifecycle, and difficult to access due to limited supply. Total global sales of the GLP-1 class of drugs are less than US$20bn annually, compared to a global medtech market of over US$500bn.

- Treatment cost remains high, and reimbursement is falling. In the US, the biggest market globally, these drugs cost patients up to US$1,000 per month, and insurers are cutting back coverage in response to irresponsible prescribing for recreational reasons.

- As with all drugs, there can be side effects. The risk is on a patient-by-patient case, and so far the data shows that between 20-30% of starters drop off due to side effects including nausea, vomiting and diarrhea. Additionally, there is also a signal for increased risk of thyroid cancer.

The reaction of investors to the new GLP-1s focus has caused one of the sharpest and fastest selloffs we’ve ever seen in medtech. While the drugs are certainly working, below we try to address the likely real-world effects of widespread use of GLP-1s on medical technology utilisation.

First order: blood glucose control

GLP-1s are now likely to become an early line of defense against diabetes, ahead of medtech devices. Thus, our view is that initiation of insulin pump therapy will likely be delayed in most patients, and some may now not ever require said pump if their blood sugar can be managed effectively by GLP-1s. The results of a recent survey of 20 high volume diabetes clinicians conducted by Piper Sandler showed that the clinicians expect only 5% of patients currently on a pump to come off, and 30% to delay starting on a pump. This data aligns with our perspective: for many patients, the course of their condition is already predetermined.

However, we think that GLP-1s are unlikely to have much impact on monitoring of blood sugar via continuous glucose monitoring devices, because physicians will always remain interested in tracking patient health data. Therefore, the biggest players in this space (Dexcom, Abbott and Medtronic), are less likely to be impacted in the short to medium term, as clinicians continue to monitor these metabolically unhealthy patients to guide treatment.

Second order: weight loss

We see a significant negative impact on the volume of weight loss (or bariatric) surgeries performed as more obese patients are prescribed and benefit from GLP-1s. Companies who generate revenue from bariatric surgery technology, including Teleflex, Intuitive Surgical and Medtronic, will likely see contraction in these relatively insignificant revenue streams. Teleflex management confirmed as much on their most recent earnings call.

Finally, as excess weight is one of the more common causes of sleep apnea, if GLP-1s are successful over time, there is likely to be slower growth in the total addressable market (TAM) for sleep apnea devices provided by the likes of ResMed, Philips and Inspire Medical. However, while these drugs have the potential to impact long-term TAMs of companies like ResMed, the vast majority of their 160+ million customers will remain on the platform buying high-margin consumable masks, and the new pipeline of patients will not be cured overnight.

Third order: reduced risk of cardiovascular events due to better blood glucose and weight control

We remain very bullish on the cardiovascular medical device market in particular. The first reason has been well-articulated by Cordis Medical Advisory Chairman and active cardiac surgeon, Professor Michael Vallely: “obesity presents a huge concern when I am planning an operation, I am hopeful more patients can now safely undergo life improving and extending interventions”. The second reason is that while obesity and high blood sugar levels are indeed major risk factors for development of cardiovascular disease, an even more important risk factor is something medical science is still searching for solutions to – ageing. GLP-1s have the potential, like statins, to significantly reduce the risk of developing early on-set cardiovascular disease, but just like in the post statin world, patients being kept alive longer will require more treatments for other conditions. Life-extending treatments are in some ways delaying the inevitable, a void in which the demand for medical technology will continue to increase with the ageing population.

GLP-1s are certainly working and the demand is real, but given the nascence of the market we remain very positive on the near and mid-term outlook for current standard of care treatments – including medical technology. With medtech earnings power to persist, the short-term fear driving market prices at the moment look overdone to us, even with a slightly cloudier long-term outlook as the GLP-1 market develops. The fact remains that medtech markets are still generally healthy today, procedure volume outlook is solid, margins are improving, and innovations are ample across sub-sectors.

1. https://au.finance.yahoo.com/news/statins-market-size-hit-us-122000664.html#:~:text=Statins%20have%20become%20one%20of,be%20over%20%2420%20billion%20annually, as at 1/9/23

2. Bloomberg News, accessed at: https://www.bloomberg.com/news/articles/2023-08-17/glp-1-weight-loss-drugs-ozempic-wegovy-mentioned-on-recent-earnings-calls

Disclaimer

This report was prepared by Cordis Asset Management Pty Ltd ABN 68 637 078 490 a corporate authorised representative (No. 1282680) of Avenir Capital Pty Ltd ACN 150 790 355, AFSL 405469 (“Cordis”)”, the investment manager for the Cordis Medical Technology Fund (“Fund”). Equity Trustees Limited (“Equity Trustees”) ABN 46 004 031 298 AFSL No. 240975, is a subsidiary of EQT Holdings Limited ABN 22 607 797 615, a publicly listed company on the Australian Securities Exchange (ASX:EQT), and is the Responsible Entity of the Fund. This document has been prepared for the purpose of providing general information only, without taking account of any individual person’s investment objectives, financial circumstances or needs. Whilst every care has been taken in the production of this document, no warranty is given as to its accuracy and persons relying on this information do so at their own risk. The information contained in this document is not intended to be relied upon as a forecast and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy, nor is it investment advice. Any forwarding-looking statements or forecasts are based on reasonable assumptions, but cannot be relied upon as guarantees or representation as to what future performance will actually occur. Unless otherwise specified, the information contained in this document is current as at the date of issue and all amounts are in Australian Dollars (AUD). You should consider the Product Disclosure Statement (“PDS”) in deciding whether to acquire, or continue to hold, the product. A PDS and application form is available at www.cordisam.com. Cordis and Equity Trustees do not guarantee the performance of the Fund or the repayment of the investor’s capital. To the extent permitted by law, neither Equity Trustees, Cordis, nor any of their related parties including its employees, directors, consultants, advisers, officers or authorised representatives, are liable for any loss or damage (including consequential loss or damage) arising directly or indirectly as a result of reliance placed on the contents of this report. Past performance is not indicative of future performance. The unit price performance calculation methodology follows the FSC Standard No.6: Investment Option Performance – Calculation of Returns (July 2018). Total returns are calculated based on changes in net asset values, at the exit price after the deduction of fees and expenses. Due to individual circumstances, your net returns may differ from the net returns quoted above.